Why Your Branch Manager Cannot Be Your Best Financial Advisor…?

The Gap Between Banking Relationships and Real Wealth Planning

Let me start with a small story.

Rohit walks into his bank branch to renew a fixed deposit. The Branch Manager greets him warmly. They chat about markets, inflation, and “better returns.” Within 20 minutes, Rohit walks out with a bundled insurance policy, a market linked investment plan, and a feeling that he has done something smart.

Six months later, he realizes he cannot exit without heavy charges. The “guaranteed” returns were not really guaranteed. And the product was never aligned with his actual goals.

The Branch Manager was not evil. He was doing his job.

01

Targets Drive Behavior

A Branch Manager is not just a financial guide. He is also a sales head for that branch.

He has targets. Deposits, Loans, Third party products, Insurance, Mutual funds, Cross sell ratios, Quarterly numbers, Year end pressure.

When incentives and promotions depend on product sales, advice automatically tilts toward what the bank wants to push, not necessarily what you need.

Even a well intentioned manager operates inside a system designed to sell.

02

Conflict of Interest Is Built In

A true financial advisor should ideally work for you.

A Branch Manager works for the bank.

That difference matters.

If your goal is early retirement, optimal asset allocation, tax efficiency, or disciplined long term compounding, you need advice that is unbiased. You need someone who is not compensated differently based on what you buy.

03

Insurance Products Often Fall Short

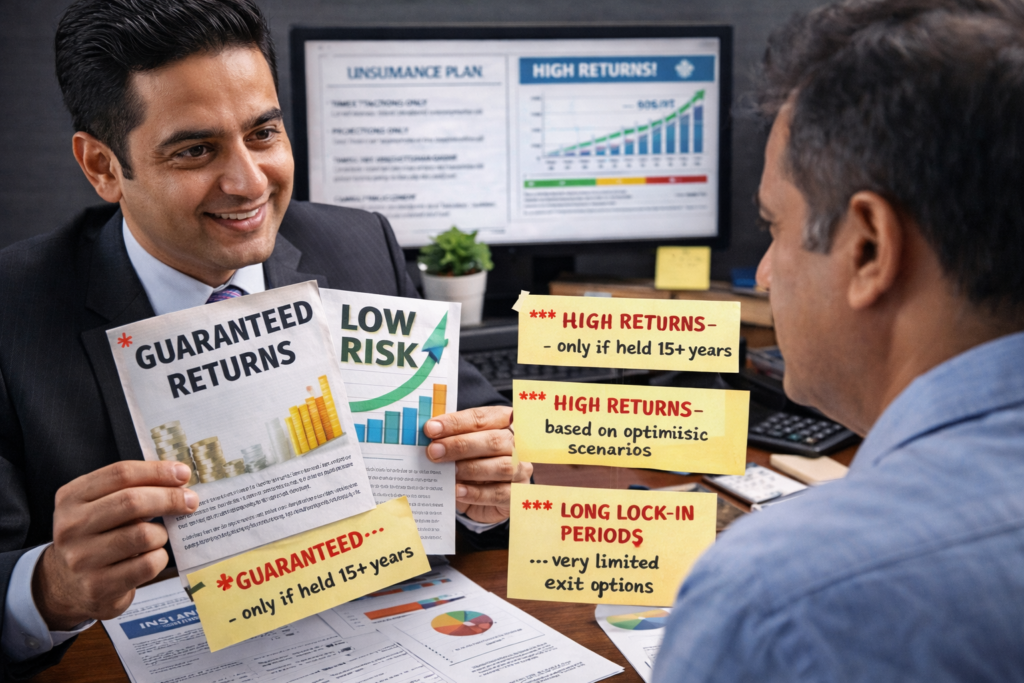

Let’s talk about insurance.

Many bank sold insurance products are bundled, complex, and expensive. Traditional endowment plans, money back policies, and certain ULIPs often promise safety plus returns. But when you break down the numbers, the internal rate of return is usually modest.

Pure term insurance is cheaper and more efficient for protection. Low cost mutual funds are often better for wealth creation. But these products usually generate lower commissions compared to bundled insurance plans.

So what gets sold more aggressively?

You already know the answer.

03

The Mis-selling Problem

Mis-selling is not always a blatant lie. Sometimes it is selective information.

“Guaranteed” may mean guaranteed only if you stay for 15 years.

“High returns” may assume optimistic projections.

“Low risk” may ignore liquidity lock-ins.

The average customer trusts the authority of the Branch Manager. After all, he sits in the cabin, handles large accounts, and speaks confidently about markets.

But confidence is not the same as fiduciary responsibility.

What Should You Do Instead?

Use your bank for what it does best. Safety, transactions, credit, basic deposits.

For financial planning:

1. Understand your goals clearly.

2. Separate insurance from investment.

3. Question every lock-in and every guarantee.

4. Compare products outside the bank ecosystem.

And most importantly, never invest out of relationship pressure.

The Branch Manager may be your friend. He may attend your family functions. He may genuinely care about you.

But he operates within targets, pressure, and product mandates.

Your money deserves advice that is free from those compulsions.

In finance, relationships are warm. Numbers are cold.

Always let the numbers win.